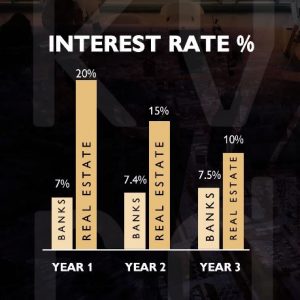

Again, building on the assumption that you’d invest 1 million into a 15% stable interest rate savings bond for three years. In 2022 upon liquidating your bond, the amount total would be 1,450,000 EGP. Now to understand the real vs. nominal interest rates equation, we’ll look into buying power of the invested 1M in 2020 and as 1.45M in 2022.

In 2020; 1M can buy you a real estate property that appreciates annually at an average rate of 20%, then 15% in 2021, and a capped forecasted rate at 10% for 2022, which would be higher than the real interest rate you’d get annual in a bank. Or 1M can buy you a commercial office or clinic space property that appreciates annually at an average rate of 15%, which is double the real interest rate in banks. But if you were to wait and try to buy a residential or commercial property in 2022, you wouldn’t be able to buy the same size or facilities for 1.45M. That is because the real estate market appreciates at a much higher rate and accounts for inflation.